Not So Deep Dive: Yeti Holdings (Ticker: YETI)

Not So Deep Dive: Yeti Holdings (Ticker: YETI)

Does this outdoor brand have durability?

Research folder with show notes, charts, and valuation: https://drive.google.com/drive/u/0/folders/11tXqAxrmTEhMorMjgIyQpa9iZWQf11ee

As always, listen to the episode on Spotify, Apple Podcasts, or wherever you are subscribed to the show.

Show Notes and Charts

(Ryan) What they do: Yeti designs and distributes popular outdoor products that it sells through both direct-to-consumer (online and through its own stores) and wholesale channels. Yeti classifies each item into one of three product categories.

Coolers and Equipment: This segment includes hard coolers, soft coolers, cargo, bags, and tons of other outdoor living accessories. These items are sold at a premium price ($375 for the base model of their largest hard cooler) and most of the items are customizable. “Coolers & Equipment” accounted for 39% of sales in 2021.

Drinkware: The drinkware segment consists of a family of drinking products that are all made with stainless steel and designed for “No Sweat”. These include Tumblers, Bottles, Mugs, Jugs, and more. “Drinkware” accounted for 59% of sales in 2021.

Other: This segment encompasses a variety of YETI-branded gear including shirts, hats, bottle openers, and plenty more. “Other” accounted for 2% of sales in 2021.

Yeti’s marketing and product development teams work together to identify and design new products. Once items have been verified to go to market, Yeti partners with third-party manufacturing and logistics partners to build and distribute their products. They have a diverse set of manufacturers located all around the globe to minimize supply chain concentration risk.

(Ryan) History: Yeti was founded in 2006 by two brothers, Ryan and Roy Seiders, who were born and raised in Austin, Texas. The two brothers attended college in their home state and worked briefly at companies that manufactured outdoor goods. Growing up as avid outdoorsmen, Ryan and Roy spent a lot of time fishing and were frustrated by their coolers breaking when they tried to use them as a standing mount for casting a line. That sparked their goal of building the world’s most durable cooler. This hard-side cooler ended up being a huge success despite a lofty price point and became a staple of hiking and fishing culture.

From there, they expanded the sales reach of their cooler business and in 2013 they introduced their first drinkware product, the Rambler. This gave a different customer cohort an introduction to the brand at a cheaper price point. In preparation for going public, the company brought in Mattew Reintjes as CEO in 2015 to take over from Roy Seiders. They ended up delaying the IPO that was originally planned for 2016 and instead opted for a 2018 debut. The stock is now about triple its IPO price.

(Brett) Industry/Landscape/Competition:

With its self-described market as “innovative outdoor products,” I’m going to look at the entire outdoor products market

The industry was estimated to be $54.1 billion and third-party analysts expect it to grow to $82.6 billion by 2028. Almost every study claims an industry will grow, so take this with a grain of salt, but in general, the outdoor products market has seen increased spending.

However, right now Yeti only operates in a subsection of these markets

Coolers: Global camping cooler market is estimated to be around $1 billion a year

Drinkware: The reusable water bottle industry was valued at north of $8 billion a year

These are not perfect metrics for Yeti’s current TAM but can give a ballpark of what they are going after

Competitors: Igloo, Coleman, Pelican, Otterbox, HydroFlask, CamelBak. Generally, they are trying to get middle-class and above people to upgrade to premium coolers, drinkware, and more.

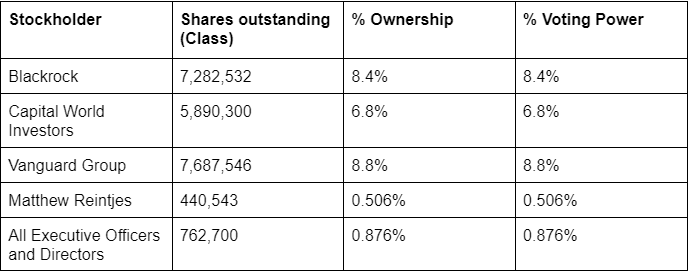

(Brett) Management, Ownership, Compensation:

CEO is Matt Reintjes. He was appointed in 2015 and had previous experience at Danaher for a decade. 46 years old.

The Chairman of the board is Robert Shearer, who was a long-time executive at VF Corporation which owns North Face, Timberland, and Altra.

Executives are paid short-term incentives based on sales and adjusted operating income targets. Long-term stock awards are extremely convoluted and based on three-year free cash flow numbers, total shareholder returns, and other stuff. Some awards are granted with no requirements except keeping your job.

The adjusted operating income and sales growth targets were 19% in 2021

Total board compensation was $1.27 million in 2021 or 0.16% of total gross profit

Total executive officer compensation in 2021 was $16.1 million, or 1.97% of total gross profit

Yellow flag: they hire a compensation consultant. Green Flag: They prohibit the repricing of stock options.

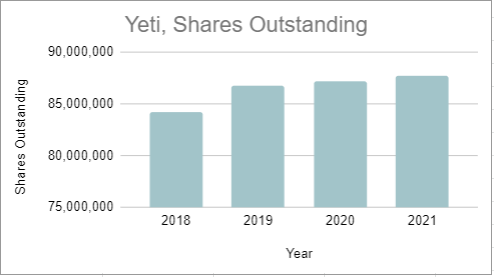

(Based on 87,051,652 shares outstanding as of 2022 Proxy)

(Ryan) Earnings:

Last 12 Months:

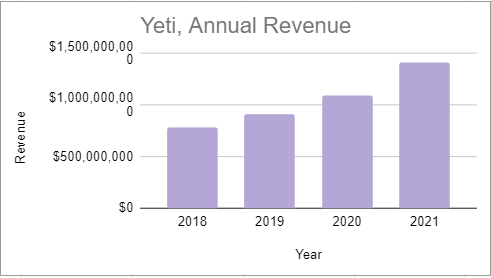

$1.5 billion, up 19% compared to the 12 months prior

55% gross margins

17% operating margins

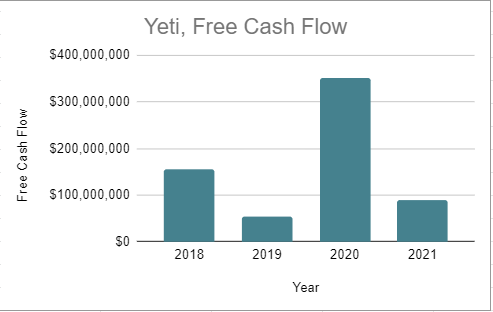

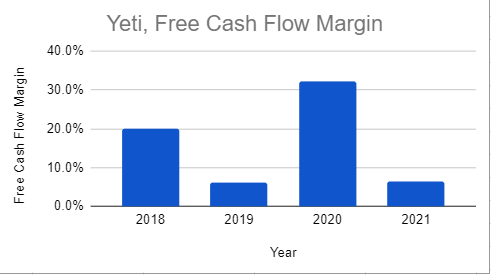

Cash flow has been diminished due to replenishment of inventory

Most recent quarter:

$420 million in revenue, up 17% YoY

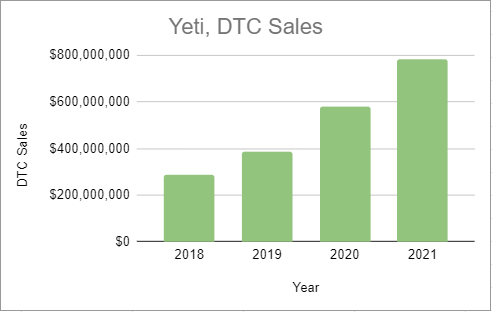

Direct-to-Consumer grew 14% to reach $225 million

Wholesale grew 21% to reach $195 million (inventory levels were understocked previously, which led to the higher growth rate)

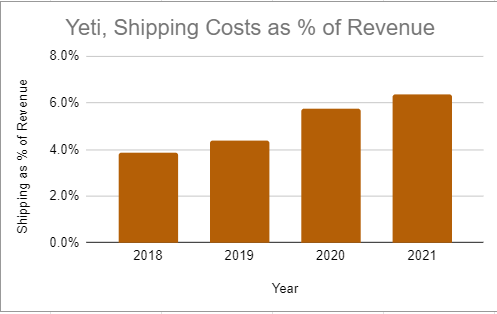

52.2% gross margin vs. 58.5% last year (fuel/freight costs, higher product costs, and foreign exchange impact all hurt gross profit)

$68.3 million in operating income vs. $72.4 million last year

Negative $75 million in operating cash flow (inventory levels increased by 121%)

Spent $26 million on capex (mix of new product building and new store openings)

(Ryan) Balance sheet and liquidity:

$91 million in cash and equivalents

$108 million in total debt ($25 million is due in the next 12 months)

$490 million worth of inventory vs. $222 million last year

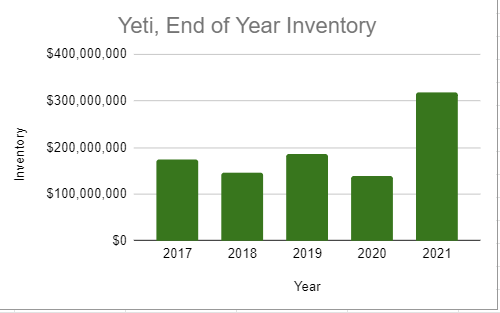

Inventory units grew by 70%

Most of the inventory growth came from coolers and equipment, which has been constrained relative to historical levels.

“We are actively managing our purchase orders with our suppliers to reflect updated demand expectations”

(Brett) Valuation: Based on a stock price of $44.47

Dynamic valuation: https://docs.google.com/spreadsheets/d/1DkqrbNGmz2x8LiwqlnLpbeMuYazxsl2dUNz_psRa_Zo/edit#gid=1158224439

Enterprise value of $3.8 billion

EV/OI of 14

EV/FCF of 42.5

Both are based on 2021 financials

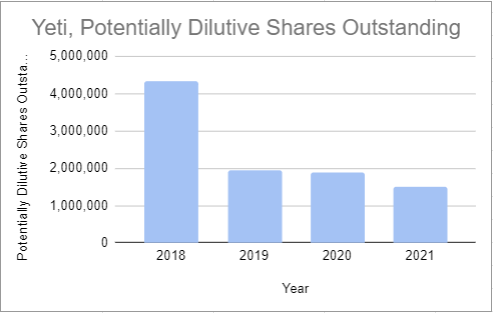

Potentially dilutive securities of 1.5 million vs. 86 million shares outstanding. This ratio has been going down the past few years.

Anecdotal Evidence:

(Ryan) I believe I’ve got a few of these products as gifts before. I’m a little indifferent about the drinkware category, but I’ve actively searched for some of their apparel purely because of the brand.

(Brett) I would buy the product if I was looking for something that would last for 10 years. They have really captured that distinction as the premium brand for their niche.

Future growth opportunities:

(Ryan) International growth. So far, Yeti has expanded its presence into Canada, Australia, New Zealand, Japan, and Europe. Last year, international revenue accounted for just under 10% of sales but was growing by 102%. The blueprint here is to get connected with prominent wholesalers first before establishing any owned stores. Diversifying geographies helps diminish the risk that the brand can lose prominence.

(Brett) Flagship stores. They currently have 13 open in the south, Texas, and Southwest of the United States. These have great reviews and have a similar concept to what RH wants to achieve with its clients (although likely with a less expensive roll-out). Here’s a review on Google Maps: “So rare to see brands behave like this, literally sell mugs and coolers but I was DYING to spend because of the perfect story being told throughout the store. As a consumer, YETI hit my whole story, even down to my dog.”

Highlights and lowlights:

Ryan’s Highlights:

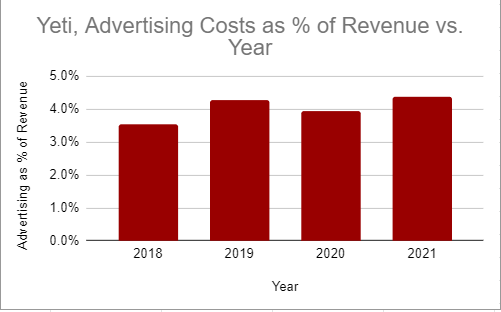

I like their marketing strategy. They’re really focused on telling a story with the Yeti brand, similar to Nike’s model. This often means spending on stuff that doesn’t have a clear return-on-ad-spend but pays off in other ways. Helps with expanding to new products.

For example, this quarter there was a viral user-generated content series where customers posted videos of YETI products surviving crazy conditions. Hard to say how much sales that specifically drive, but you know it’s good for the brand.

The successful transition to a largely direct-to-consumer model demonstrates how much people love Yeti. They aren’t seeking out coolers, they’re seeking out Yeti coolers.

Ryan’s Lowlights:

I don’t like brand-driven moats unless they’ve either been around for 40+ years or sell an unhealthy addiction (caffeine, nicotine, sugar, salt, etc.). Consumer sentiment can change fast and I think that’s still a real risk for Yeti today.

Brett’s Highlights:

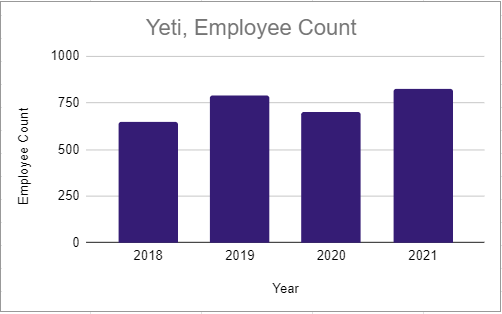

My biggest highlight has to be management. It is tough to get a full grasp on a strategy within a week but there were some things I liked, including long-ish tenure, Danaher pedigrees from two executives, reasonable compensation and SBC expenses, reasonable employee count and expense structure, share repurchase strategy, and solid operating targets for yearly bonuses.

The brand quality is strong, and management seems to have learned from the other strong American brands like Apple, Nike, etc. in advertising strategy. If/when more stores open up, brand awareness and quality should only grow.

International expansion has been incredibly strong and the brand (especially drinkware) should travel well in many markets.

Brett’s Lowlights:

The cash conversion and inventory will always be a concern here. A quality business consistently turns profits into cash flow, and Yeti hasn’t proven it can do that yet. The pandemic may have made things difficult, but this is still a concern, especially right now.

Another concern I have is with how recurring a customer purchases products. Both drinkware, coolers, and even bags are meant to be purchased once every five years. This is fine if everything costs $300 and the customer comes back again, but it makes the business lower quality than apparel from my point of view.

Bull Case:

(Ryan) Yeti continues to roll out new products as well as new iterations of existing products to support stable growth domestically and the brand gains similar traction abroad. I think at these prices, if Yeti can grow revenue by 10% a year over the next 5 years and cash flow margins revert back closer to EBIT margins (15%-20%), this will generate good shareholder returns.

(Brett) Given the really solid expense structure, I wouldn’t be surprised if this business can achieve 22% - 23% operating margins when shipping costs come back down to earth. At the current EV/OI of 14 (based on 2021 numbers), if revenue grows at 10%+ over the next five years and management buys back stock I think it is easy to see solid returns going forward.

Bear Case:

(Ryan) Yeti is unable to maintain its spot as the premier outdoor lifestyle brand. I.e. an Under Armour-like scenario occurs. This could potentially not only lead to declining sales but margin compression as well. Hard to precisely quantify what a bearish scenario would look like for the company, but if the brand loses relevance, momentum really starts to work against them.

(Brett) My two big concerns: margin deterioration from input costs (both commodities and shipping) and the size of the addressable market. Yeti will likely have to expand into new product categories in order to continue compounding revenue, and I’m not certain they can win. Should they start trying to acquire other outdoor brands? I can think of plenty of other products at REI that could fit within their portfolio.

More or less interested?

(Ryan) More interested. But I think businesses, where the investment thesis is predicated on the staying power of a brand, deserve to trade at a discount, and I’m not sure Yeti is quite there yet.

(Brett) More interested. There are concerns with brand durability (it is unpredictable) and inventory build-up, but it is trading at a reasonable price and has executed well over the last five years.

Stock for next week? (Ryan: SiriusXM)

Sources and Further Reading

Q2 Conference Call transcript: https://www.fool.com/earnings/call-transcripts/2022/08/04/yeti-holdings-inc-yeti-q2-2022-earnings-call-trans/

Yeti’s Online Store: https://www.yeti.com/

Latest 10-K: https://d18rn0p25nwr6d.cloudfront.net/CIK-0001670592/87e205ad-45bd-4c9a-8cab-382b7328bd3f.pdf

2022 Proxy Statement: https://d18rn0p25nwr6d.cloudfront.net/CIK-0001670592/4a9fbaf0-2b24-4169-b94d-6f4e5787faec.pdf