Not So Deep Dive: Warby Parker (Ticker: WRBY)

Not So Deep Dive: Warby Parker (Ticker: WRBY)

Is this more than just a glasses company?

Research folder with show notes, charts, and dynamic valuation: https://drive.google.com/drive/u/0/folders/1_6FTCoBn47zUmPZvz_iJsGmbh9cGb1t7

As always, listen to the episode on Spotify, Apple Podcasts, or wherever you are subscribed to the show.

Show Notes and Charts

(Ryan) What they do: According to the first line on their 10-K, “Warby Parker is a mission-driven, lifestyle brand that operates at the intersection of design, technology, healthcare, and social enterprise”... They sell glasses.

Warby Parker (WP) operates an omnichannel model that sells a variety of eyewear products ranging from prescription eyeglasses to sunglasses or even contacts. And by cutting out the middlemen (3rd party retailers), they are able to sell most items at a discount to their competitors. They design their glasses at their NYC headquarters and contract manufacturing and logistics partners to build and ship their products.

Online: With WP’s website and mobile app customers can easily browse and purchase eye care solutions and have them shipped to them. To ease the burden of buying online, WP offers free At Home Try-Ons and Virtual true-to-scale Try-Ons. Customers can also receive a virtual vision test to receive a prescription.

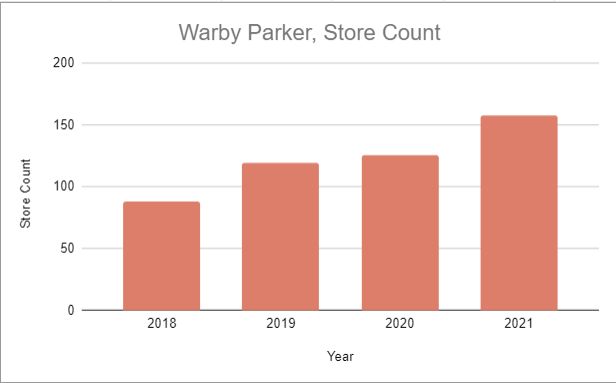

In-person: WP has 169 physical company-owned retail locations scattered across the US (with 3 in Canada). At the majority of these stores, Warby Parker has hired optometrists to help conduct in-person eye exams for customers. Retail locations also serve as good marketing and brand building. (e-commerce sales growth in the geographies with retail locations).

(Ryan) History: Warby Parker was started by four friends (Neil Blumenthal, Dave Gilboa, Andy Hunt, and Jeff Raider), who were attending Wharton school of business at the time. The idea was sparked with all of them complaining about the cost of replacing their glasses. They figured out that most eyewear brands were owned by Luxottica and thought it was a market ripe to be disrupted. They pitched it in a business class competition but failed to win. So they ended up starting the company with all of their own money ($120k in total). This money gave them enough funds to hire a manufacturing partner and a PR firm to get the word out.

The model was initially entirely online and the glasses cost $95. And after being featured in GQ and Vogue magazines, the orders began to roll in. From there the company raised several rounds of funding and was able to find some early product market fit. By 2015, the company was valued at $1.2 billion, and in 2020 the company raised a Series F and Series G round valuing them at $3 billion. In September 2021 they went public via a direct listing and today they sit at a $1.4 billion market cap.

(Brett) Industry/Landscape/Competition:

(The majority of these metrics are from Warby Parker’s own estimates)

The U.S. eyewear market is valued at $44 billion a year. This and Canada are the only countries Warby Parker says they are going to focus on for a long time.

The global eyewear market is valued at $160 billion and has been growing steadily for decades. As countries get richer, more people have the freedom to focus on things like getting glasses.

According to the 2021 10-K, only 8% of the eyeglass market is e-commerce right now

The vision insurance market is valued at $54 billion, according to IBIS World. This is a market Warby Parker wants to go after long-term.

Competitors: Two huge ones: EssilorLuxottica and VSP. EL owns brand lenses like its namesake, Ray Bans, Kodak, Transition, and many others. It also sells a lot of equipment to optometrists. It owns/sells brands like Oakley, Ray Bans, Versace, and many others. Lastly, it owns retail shops like Sunglass Hut and Vision Direct. This is the legacy player that Warby Parker management constantly talks about.

VSP is a global vision care provider with over 85 million members. Long-term, Warby Parker wants to disrupt them with its vertically integrated model.

(Brett) Management and Ownership:

Co-CEOs: David Gilboa and Neil Blumenthal. These guys are also co-founders of the company. In 2021, they got a $450k base salary, close to $100 million in stock grants, and $3.5 million in options each.

The huge stock grants come from a long-term stock grant plan based on where Warby Parker’s stock trades. The first tranche is at $47.75 a share, and the last tranche is at $103 a share.

The CFO is Steve Miller. He has been with the company basically since its inception. In 2021, he got $5.9 million in total compensation.

Jeffrey Raider is a co-founder but left to start Harry’s, a sizable CPG business. He still sits on the BoD today.

Outside of a member from General Catalyst, it looks like the board of directors is all made up of mercenaries (excluding the executive team).

Some members of the board are getting paid $800k - $1 million a year

Yellow flag: Annual bonuses are based on revenue and adjusted EBITDA targets

Yellow flag: Huge stock grants to executives that already have skin in the game.

Yellow flag: Blumenthal and Gilboa seem to have started a venture capital firm back in 2019.

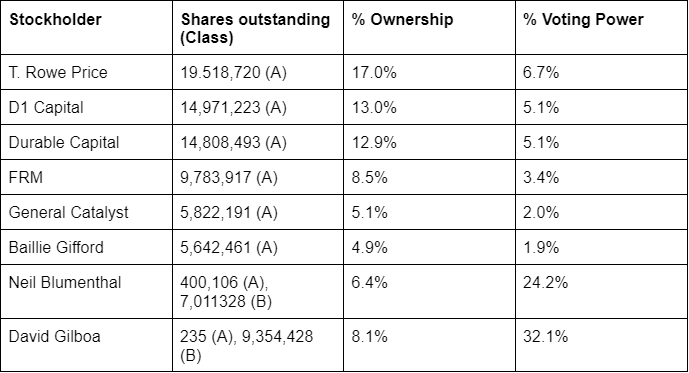

(Based on 114,942,785 shares outstanding, 2022 Proxy Statement)

Big takeaways:

Blumenthal and Gilboa have a lock on voting power

Most of the A shares are tied up with venture capital and/or venture capital-style public investing firms like Ballie Gifford

The company gives out healthy (if that is the right word) compensation to both executives and the board of directors.

(Ryan) Earnings:

Over the last 12 months:

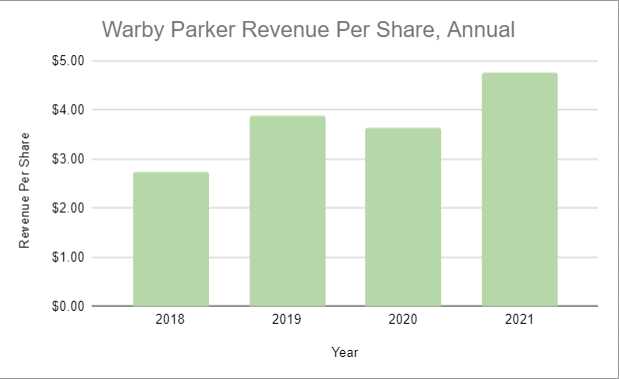

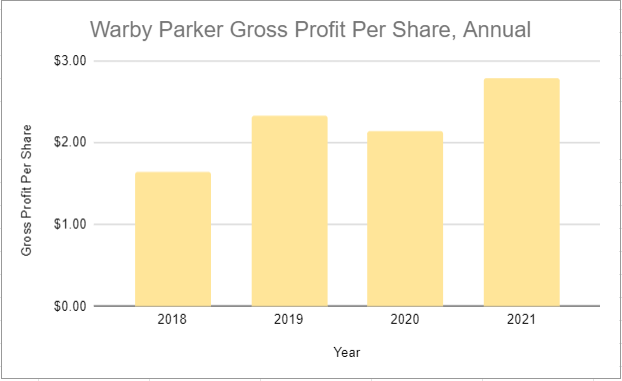

Revenue $555 million, up 25%

58% Gross Margin

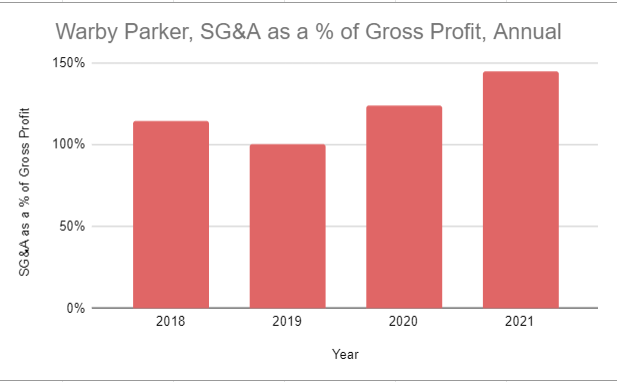

Unprofitable

Most recent quarter:

Revenue was $153.2 million, up 10.3% YoY

Had “$15 million in estimated lost sales due to omicron”

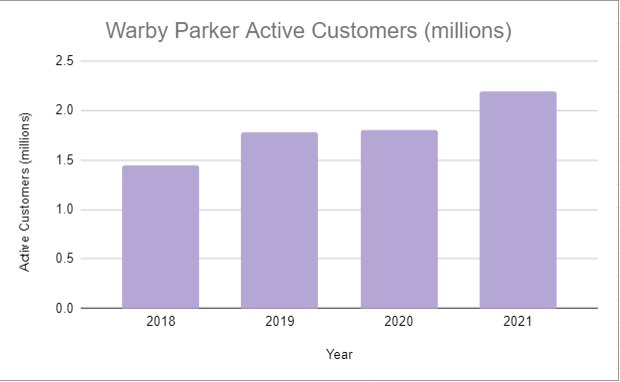

Active customers increased by 18% to 2.23 million

Opened 8 new stores during the quarter. The total store count reached 169, up 26% vs. last year.

($10.3) million in operations cash flow. $16 million in purchases of property and equipment. -$27 million in free cash flow.

(Ryan) Balance sheet and liquidity:

Very simple. Warby Parker has $230.3 million in cash and cash equivalents and no true debt.

They have $152 million in total lease liabilities. But I believe that goes to litigation over whether or not it is voided in bankruptcy, so I don’t include it in my enterprise value calculation.

Inventory hasn’t increased too much over the last year. Good sign.

They’ve burned through $95 million in cash over the last year. That’s about two and half years of cash runway at the current burn rate.

(Brett) Valuation:

Dynamic valuation: https://docs.google.com/spreadsheets/d/1SYjNX1Z2VTh1oc8KjtpYqu0uUrctJUrZcCcAEFKs7Xk/edit#gid=2018696472

Market cap of $1.4 billion, ticker WRBY

The technical enterprise value is below the market cap, but since they are cash burning I will be using price-to [blank] ratios because the cash on the balance sheet is not available to shareholders.

P/S of 2.5

P/GP of 4.3

P/OI (assuming 10% margin) of 25

11.4 million potentially dilutive securities outstanding, or 10% of current shares outstanding. Given management’s tendency to use the stock for compensation, I would estimate 3% - 5% share dilution going forward.

Anecdotal Evidence:

(Ryan) I saw people wearing their sunglasses yesterday. They look pretty cool.

(Brett) I would 100% use the service if I needed eyeglasses. Also, are all employees required to need glasses? That’s what it seemed like at the analyst day.

Future growth opportunities:

(Ryan) I have two. (1) Retrofitting existing stores to be able to serve eye exams. Right now 115 of their 169 stores offer eye exams. “70% of glasses wearers purchase glasses from the same place they get their eye exam”. (2) Expanding in-network insurance relationships. Even if the glasses are still cheaper out-of-network, people tend to rely on their in-network benefits. So adding those relationships should help attract customers.

(Brett) Opening more stores across the nation. They currently have 169 stores, and management believes it can get close to 1,000 in North America. According to the company, stores greatly accelerate market share gains in new markets, serve as free advertising, and retain higher paying customers. This makes sense because a lot of people likely still prefer getting their exams done in person.

Highlights and lowlights:

Ryan’s Highlights:

They look cool. WP seems to have found product market fit, and I believe their claim that word of mouth is a meaningful driver of new sales.

The pivot to a multichannel model seems to be helping drive overall sales. I like the retail model.

Ryan’s Lowlights:

The company is still being run like a venture capital business and there are red flags galore with management. I don’t think they are prioritizing minority shareholders at all.

I hate their use of adjusted EBITDA as a metric. They aren’t a software business. They’re in the process of pivoting to an increasingly retail-first model and they roll out new lines of glasses all the time, which means that depreciation is a very real cost for them. Additionally, they give out stock like its candy, so “adjusted ebitda” is nowhere near indicative of shareholders' real claim on profits.

Brett’s Highlights:

Warby Parker looks to be clearly on the right side of an “Innovator’s Dilemma” battle. With the business model they’ve set up, they can profitably offer much lower prices to attract customers, but the legacy players are still unwilling to match them because it would hurt their profitability in the short run. This feels like a perfect recipe to continually gain market share.

The unit economics look solid, and with all the adjacent products they offer (mobile vision tests/try-on, stores, contacts, eye exams) it will be hard for other e-commerce eyeglass companies to compete on an even playing field.

Brett’s Lowlights:

The compensation structure for employees and executive teams seems egregious and gives me little confidence they are focused on creating value for minority shareholders. When you give out huge stock grants to founders that already have skin in the game, it makes me question where their priorities are.

The looming threat of augmented reality (AR) glasses being the next big consumer electronics product. We know for certain that Meta, Apple, and Alphabet are working on them. If these go mainstream, what happens to Warby Parker’s business? Maybe Apple would buy them but I doubt they need them to succeed.

Bull Case:

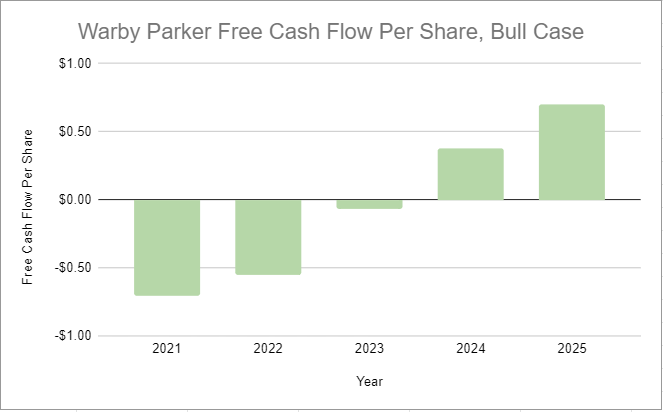

(Ryan) 15% per year active customer growth over the next 5 years. The average revenue per customer increases by high single-digit percentages each year, let’s say 7% (grew by 12% in 2021). And they reach free cash flow margins of 10%. That would leave $155 million in free cash flow. Valued at 20x, that’s a $3.1 billion market cap or a 121% increase compared to the current price.

(Brett) My bull case is fairly simple: Warby Parker continues building out its store count and sees the same sort of market share gains with the holistic omnichannel model. This leads to around 10% true operating margins (they are guiding for 20% adjusted EBITDA margins, and given their stock compensation I think this is a conservative number). Free cash flow would likely be similar to operating income once store expansion slows down. At current prices, this would likely lead to solid returns for shareholders even with 3%+ share dilution a year.

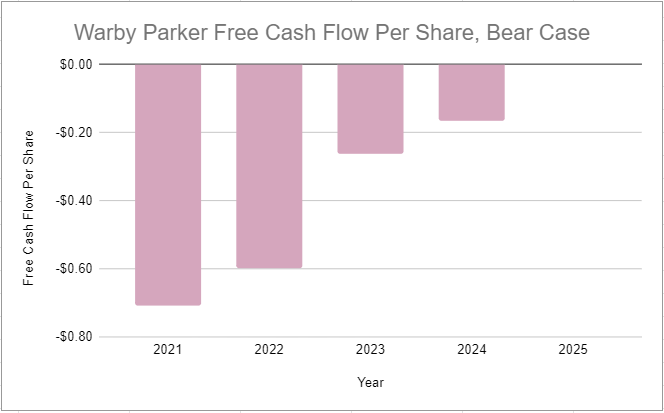

Bear Case:

(Ryan) They never get anywhere near 10% free cash flow margins and they struggle to raise money in the public markets.

(Brett) Two bear cases come to mind, and they are directly from my lowlights. First, the executive/employee/BoD compensation keeps Warby Parker from generating true profits for shareholders, even if they keep stating that adjusted EBITDA margins are positive. Second, sometime this decade Apple launches its AR lenses, crushing the traditional eyeglass market. Just look at what happened to the watch market when the Apple Watch went mainstream.

More or less interested?

(Ryan) Less interested. It feels like they could succeed and the industry seems very durable, but the management woes are keeping me away.

(Brett) I am less interested. There was a lot to like with the “Innovator’s Dilemma” and durable/growing industry, but the threat of AR glasses and management red flags is too much for me to be interested.

Sources and Further Reading

How I Built This: https://www.npr.org/2018/03/26/586048422/warby-parker-dave-gilboa-neil-blumenthal

S-1: https://www.sec.gov/Archives/edgar/data/1504776/000162828021017546/warbyparkerincs-1.htm

2021 Annual report: https://d18rn0p25nwr6d.cloudfront.net/CIK-0001504776/742c1cf1-16a0-4b49-bc36-9e2f0c37d793.pdf

2021 Analyst Day: