Not So Deep Dive: GoDaddy (Ticker: GDDY)

Not So Deep Dive: GoDaddy (Ticker: GDDY)

The crazy Super Bowl Advertiser is doing much more than investors are giving them credit for

Reminder: these are show notes that should be read in conjunction with the podcast. Do not expect these notes to be a polished research report.

December Schedule: Mercadolibre (out now), Squarespace (upcoming), Bigcommerce (upcoming), Wix.com (upcoming)

As always, listen to the episode on Spotify, Apple Podcasts, or wherever you are subscribed to the show.

Charts

Show Notes

(Ryan) What they do: GoDaddy is the world’s largest domain registry and website hosting platform. They break the business down into 2 reporting segments:

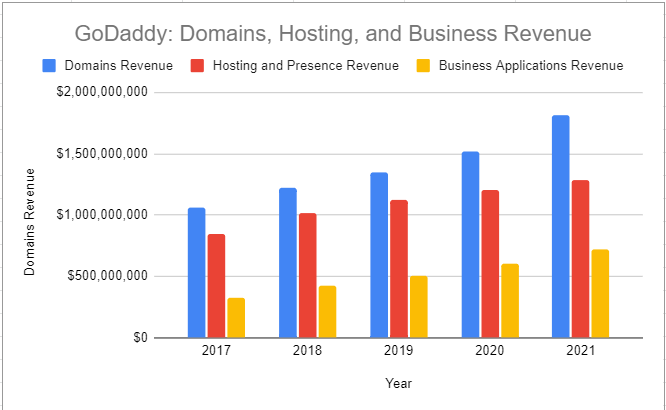

Core Platform: This consists of domains and web hosting. Combined these two accounted for 81% of revenue in 2021.

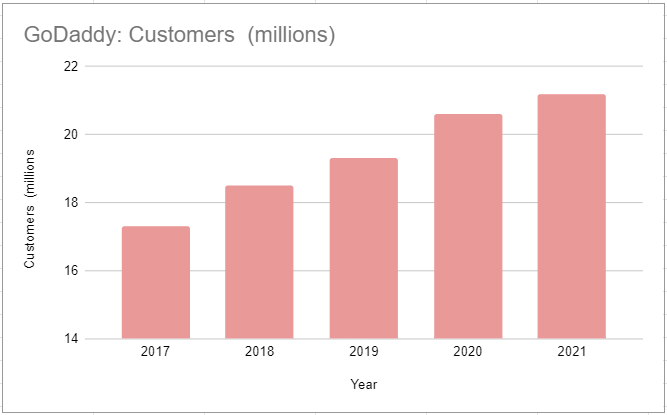

Domains: If you think about a website like a house, the URL or domain name is the land on which that house sits. GoDaddy helps customers find and secure the right domain name for them and they also help facilitate transactions if the domain is already owned. GoDaddy has more than 84 million domains under management or 23% of all domains registered worldwide.

Hosting: In addition to the domain business, GoDaddy offers website hosting services. This includes things like data storage at their various data centers around the world, security, and even content management systems. Their CMS solutions consist of both their own do-it-yourself website builder as well as Managed WordPress (one of the largest parts of the business). MWP allows customers to use an integrated WordPress building platform in conjunction with GoDaddy’s hosting services. For reference, about 10% of WordPress websites are hosted by GoDaddy.

Applications & Commerce: On top of just the design and functionality of a customer’s website, GoDaddy offers solutions to help its customers better run their businesses. These solutions consist of both in-house products as well as distribution of third-party applications. For example, GoDaddy helps customers set up Microsoft 365 accounts with their own custom domain name as well as other email accounts. Additionally, GoDaddy offers online store integrations, GoDaddy payments, and even physical point-of-sales systems.

(Ryan) History: GoDaddy was founded in 1997 by a man named Bob Parsons. Parsons is pretty unique, so it’s worth giving his background some time. Parsons grew up poor in Baltimore and reportedly almost flunked out of high school but ultimately ended up joining the Marines. After several years serving, Parsons attended and graduated from the University of Baltimore with an accounting degree and started a career in IT and Software sales. While he was still working at his job, he began to develop a home accounting program called MoneyCounts in his spare time. After 3 years working at it, he left his job and started selling this software full-time, eventually naming the company Parsons Technology. He ultimately sold the business to Intuit for $64 million in 1994. Shortly after, Parsons used the money to start a new company that would come to be known as GoDaddy.

The business was initially named Jomax Technology, but the company had a name brainstorming session and decided to name the company GoDaddy (they tried Big Daddy at first but it was taken). It’s hard to tell what exactly drove their success versus other domain registries, but by 2005 they were the largest accredited registrar worldwide. In 2011, 70% of the company was sold to a private equity consortium and in 2015 the company debuted on the NYSE.

(Brett) Industry/Landscape/Competition:

The web domain registration industry was estimated to be valued at $8.1 billion and grew at a 4% CAGR from 2017 - 2022

The non-open source (so non-WordPress) website-building market is actually much smaller than you think. The estimates from third-party analysts were too low from what I could find, but it is probably closing in on $5 billion a year. From my seat, there is no reason why website building should be a smaller industry than domain registration.

Competition within domains: GoDaddy is the leader and only competes with small players like Donuts, Automattic, Newfold, and WP Engine (although companies like Wix and Squarespace have an integrated solution)

Competition within website CMS: The leader is WordPress, and then within integrated CMS there are the big 3: Shopify, Wix, and Squarespace

WordPress has steadily lost market share this decade, which has left the door open for companies like Wix, Squarespace, and increasingly GoDaddy to gain market share

(Brett) Management, Ownership, Compensation:

CEO is Aman Bhutani, who was brought in to manage the business in 2019 after the PE firms started to fully sell their stakes (lives in Seattle, shoutout). Bhutani previously worked at Expedia for a long time period before joining GoDaddy

There are nine members of the board, with the majority being independent current or ex-executives from the software market. Total board compensation was $2.56 million in 2021 or 0.1% of gross profit. No concern about overpaying the BoD.

Executive compensation was $36.2 million in 2021 or 1.5% of gross profit. No concern about overpaying the executive team

Executive compensation is, you’ll never guess, based on a base salary, short-term annual bonuses, and long-term stock awards

Short-term bonuses are based on bookings and unleveraged free cash flow targets. Both check out to me as solid metrics to track every year

Long-term stock awards are based on a total shareholder return hurdle vs. the Nasdaq Internet Index, while there are also some non-performance RSUs as well. The TSR target is unlocked if they are at 50% median percentile of returns in the index

I think the TSR hurdle is fine, but not great. I would much rather look at some three-year growth in FCF/s or something like that

No major red flags from the Proxy statement from what I could find.

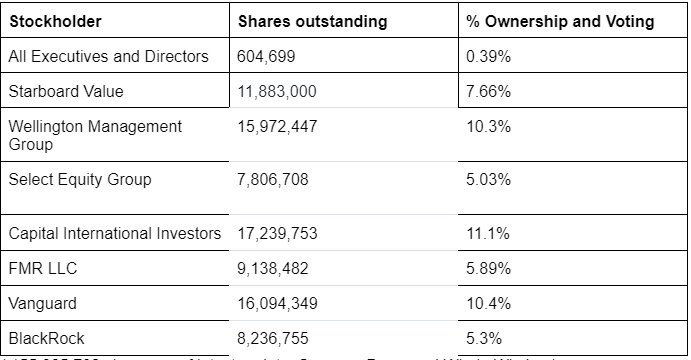

Interesting note: 40% of shares are held by non-passive investment funds (listed below)

( 155,065,792 shares as of the latest update. Sources: Proxy and Whale Wisdom)

(Ryan) Earnings:

Last 12 months:

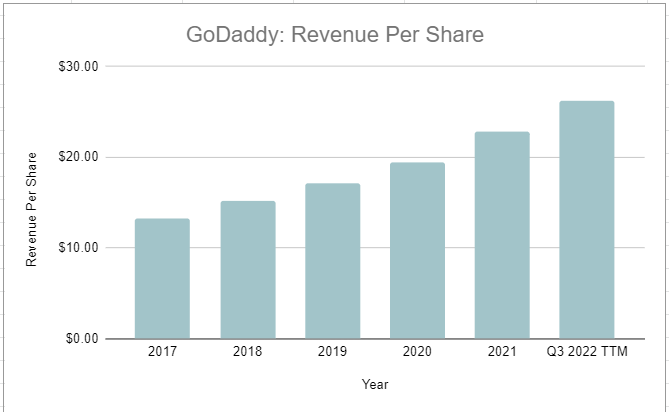

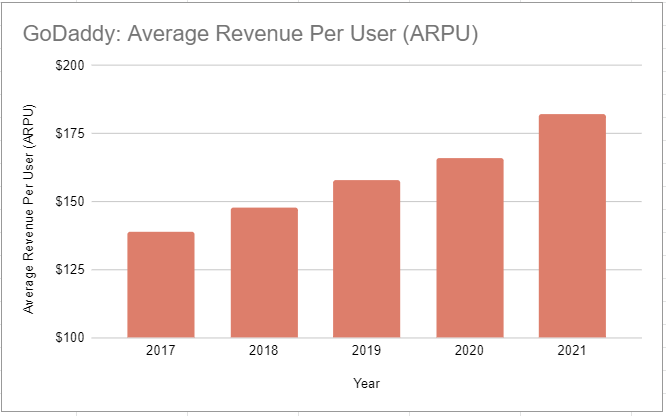

$4.1 billion in revenue, up 11%.

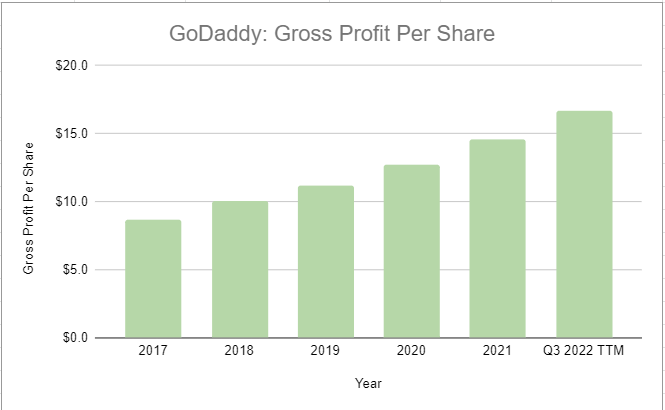

64% gross margins

$884 million in free cash flow or 22% FCF margins

Most recent quarter:

$1.03 billion in total revenue, up 7% YoY (9% in constant currency – 32% of revenue comes from outside the US)

Core Platform ARR grew 2%

Applications & Commerce ARR grew 10%

$257.5 million in true free cash flow (they report an unlevered number), up 18% YoY

13% operating margins

10% of revenue is spent on marketing & advertising. That’s significantly less than Wix, Squarespace, and Shopify.

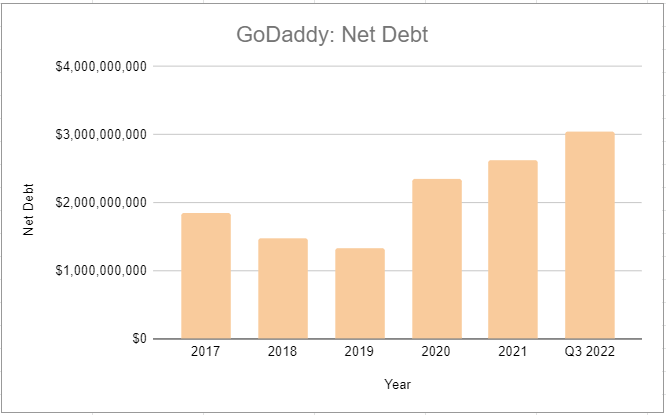

(Ryan) Balance sheet and liquidity: They do a pretty good job explaining the debt in their filings.

$826 million in cash

$3.9 billion in long-term debt, consisting of two layers, Term loans (variable) and Senior Notes (fixed).

$1.8 billion in 2024 term loans, an effective rate of 3.2%.

$733 million in 2027 term loans, an effective rate of 3.6%.

Both term loans accrue interest at LIBOR + 1.5 & 2. However, in conjunction with both term loans, they entered into interest rate swaps. This has helped keep the effective rate down.

$600 million in 2027 senior notes, fixed 5.25% interest rate.

$800 million in 2029 senior notes, fixed 3.5% interest rate.

So $3.1 billion in net debt at an attractive cost vs. $1.1 billion in unlevered free cash flow expected this year.

Net debt/FCF of less than 3x. (net debt?)

(Brett) Valuation:

Market cap of $11.8 billion

Enterprise value of $14.95 billion

EV/s of 3.7

EV/GP of 5.8

EV/FCF of 16.9

Anecdotal Evidence:

(Ryan) Honestly, they have a pretty solid brand. Definitely feels like the first place to go to reserve a domain and host a website if you aren’t doing it through a SaaS CMS provider.

(Brett) I can’t come up with anything interesting to note, which I think says a lot. Most people would recognize the name (Super Bowl commercials will do that) but don’t really care about the brand.

Future growth opportunities:

(Ryan) The logical growth avenue here is continuing to invest in their business solutions. They’ve done a good job adding functionality here for their customers so far. But my other more far-fetched growth opportunity would be to buy a better SaaS CMS platform. Their DIY solution is the one thing that’s really lacking here and it would give them less dependence on the growth of WordPress.

(Brett) Acquisition of Poynt. Poynt was a payments provider for small businesses that included point of sale, loyalty and rewards, invoicing, and other features. It did $16 billion in GMV at the time of the transaction and is now called GoDaddy Payments. Upselling its domain/website SMB customers to a payments solutions can increase lifetime value significantly. Last quarter, annualized GMV at GoDaddy hit $29 billion, and I think will be a key metric to track for investors over the next few years.

Highlights and lowlights:

Ryan’s Highlights:

Strong brand and they just continue to grow. WordPress is still the dominant solution in website building and GoDaddy’s done a good job hitching their wagon to them. I expect the core platform will eventually just grow in line with the GDP of the internet.

Seems like the upsell opportunity for applications and commerce solutions should be high. As they continue to add products there, I imagine that should continue to outpace core platform growth.

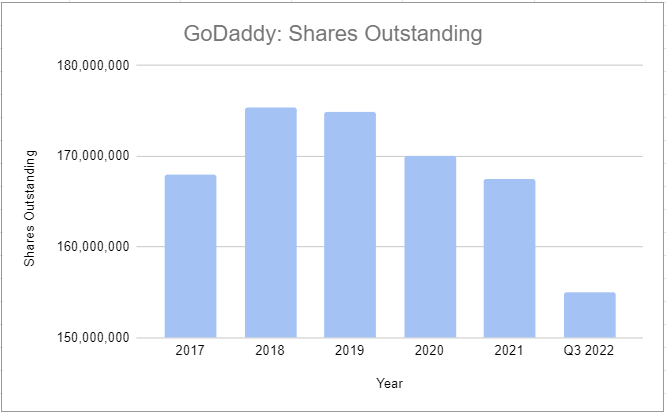

Low-cost debt is being used to acquire shares at a high FCF yield. Love that, particularly when the business looks sustainable.

Ryan’s Lowlights:

Verisign price increases. Thanks to its current contract with the internet corporation for assigned names and numbers, has exclusive registration rights for the .com gTLD through 2024. In that contract, they get to raise prices by 7% per year in the last 4 years of each 6-year contract. Those cost increases either have to be passed through or absorbed by GoDaddy. Fees paid to them account for >20% of GoDaddy’s total costs.

Website building overall is increasingly moving to SaaS CMS as opposed to just pure CMS, and I don’t think GoDaddy’s Website + Marketing DIY solution is that well positioned versus competitors in the space. Over the last decade, active CMS websites 10x’d, but the percentage of those websites that were built with SaaS CMS went from 18% to 37%.

Brett’s Highlights:

My number one highlight is management’s focus on growing free cash flow per share, which is a rare find of businesses we have looked at on the show. This, along with the levered buyback program can be a great driver of shareholder returns and I think they understand capital allocation from a minority shareholder’s perspective.

The expansion into website building has been strong as they were fairly late to the game vs. others. Now, as the domain/site provider for a lot of SMBs, GoDaddy has a ton of optionality to offer new features to customers. As well, the website-building business is moving off of traditional WordPress hosting, which should benefit someone like GoDaddy.

Brett’s Lowlights:

The domain business, while solid for GoDaddy, is much more of a commodity than website building. Yes, they have retained market share for over a decade and are the experts in the space, but I have a slight worry that they could lose market share if people don’t go to them first when setting up an online business (for example, we did everything for our fund website through Wix).

Reviews for GoDaddy’s e-commerce tools are weak. “If you are serious about e-commerce, you will outgrow GoDaddy quickly.” I worry about what value proposition GoDaddy can give to SMBs vs. a Wix, Squarespace, or Shopify which are years ahead in capabilities for website building. Are they just attracting easy customers from the domain business, or is this truly a competitor to the big 3 website builders? I don’t know.

Bull Case:

(Ryan) Let's put some numbers on it. If Core Platform ARR grows by 7% annually, Applications & Commerce ARR grows by 10% annually, and the free cash flow margin reaches 25%, GoDaddy would generate $1.3-$1.4 billion in free cash flow within 5 years. Assuming they continue using their FCF to buy back shares, that’s probably high teens FCF/Share growth. I imagine the upside on the stock here is similar.

(Brett) At the current earnings multiple, I think it would be hard to lose money three years from now if they keep up this current growth rate and repurchase stock consistently. In order to think about hitting double-digit returns, I think you need to be confident that this business deserves a premium earnings multiple.

Bear Case:

(Ryan) I think the bear case is pretty limited here. Underwhelming growth from both Core and Apps/E-comm, coupled with little margin expansion, shares will probably slightly underperform the market. Don’t see this losing money over the next 5 years though.

(Brett) My bear case is no/low growth as they stop attracting easy customers from the domain business for websites/e-comm/payments and lose to the more robust options like Wix, Squarespace, and Shopify. In this scenario, if revenue growth slows I think the earnings multiple would compress and the stock might go nowhere five years from now. I think a good sign though is that I had trouble coming up with this bear case and do not have confidence in it. But that could be false confidence from not understanding the business deeply enough.

More or less interested?

(Ryan) More interested. The core platform seems extremely consistent and I think there’s a good chance they grow FCF/share by 10% over the next 3-5 years. However, the valuation’s a little above where I’d feel compelled to buy.

(Brett) More interested. I am attracted to the website building space given the steady decline of WordPress, but there are some concerns for me about the competitive position and what that means for future growth vs. Wix, Shopify, Squarespace, etc.

Stock for next week? (Squarespace)

Sources and Further Reading

GoDaddy 2022 Investor Day Slides: https://s23.q4cdn.com/406380394/files/doc_presentations/2022/GoDaddy-2022-Investor-Day-14.pdf

2021 VIC Writeup GoDaddy: https://www.valueinvestorsclub.com/idea/GODADDY_INC/0886980680

YouTube video on GoDaddy Managed WordPress:

What is web hosting YouTube video:

GoDaddy Website Building Review 2022 (All competitors on this site as well): https://www.sitebuilderreport.com/godaddy-review